hapabapa/iStock Editorial by means of Getty Images

Today I want to go over an outside clothing business that been around given that the 1930’s. This historical business has actually increased tremulously under the period of it’s veteran CEO.

Nevertheless, the last 5 years have actually been rough as the business has under-performed the marketplace and like numerous merchants has actually had a hard time handling stock.

That company is Columbia Sportswear Business! Let’s go into the information to see if this business is poised for a resurgence.

The Business

Columbia Sportswear Business ( NASDAQ: COLM) is a leader in offering outside clothing, shoes and devices. The business was established in Portland, Oregon back in the late 1930’s and is still going strong. Columbia has an intriguing backstory as the business has actually been run by one household given that creation. The business’s existing CEO is Tim Boyle who started operating at Columbia in 1971. Tim’s grandpa and dad had formerly run the business. Performing along with his mom, Gret, Tim assisted turn the having a hard time business into a powerhouse. Tim has actually been at the helm given that 1988 and his child Joe is the existing Columbia Brand name President.

Columbia’s 4 primary brand names are Sorel, Mountain Hard Use, prAna and the initial Columbia brand name. The numerous brand names have various objectives, however all are fairly comparable to the primary Columbia’s brand name objective which is to, “ Open the outdoors for everybody.”

Maturing in the West, I am really acquainted with Columbia and have actually bought many coats and coats from the business throughout the years. I believe their clothing is really high quality and lines up effectively with the business’s objective. Their clothing is ideal for being outdoors and checking out nature.

Moat and Chance

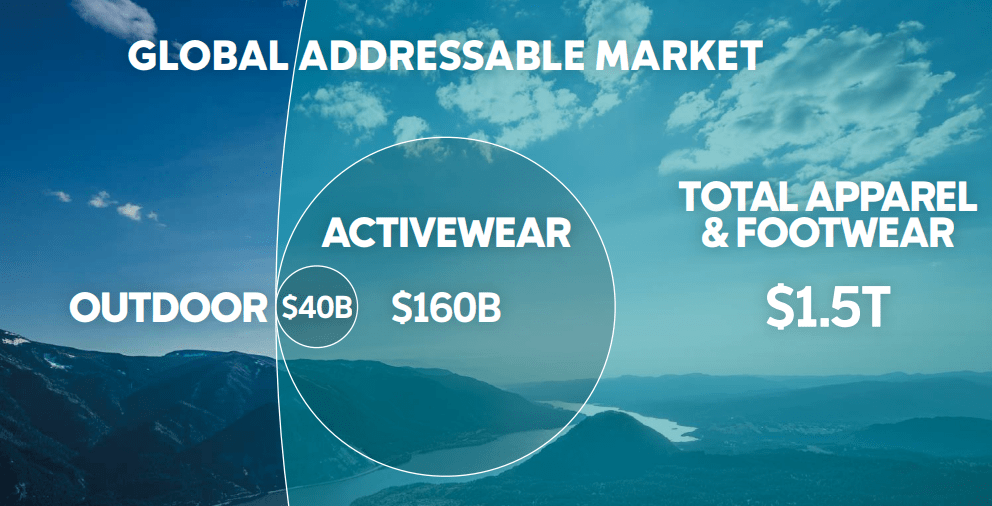

As specified on a previous financier discussion, Columbia thinks they have an addressable market of $40 billion:

Financier Discussion

Columbia’s objective is to be the top outside brand name worldwide. To arrive the business is concentrated on producing renowned items, driving brand name engagement, improving customer experiences, and enhancing market quality. In checking out the business’s financier discussion, it was difficult to get any genuine compound on how the company was going to carry out on these objectives.

I do not think Columbia has a moat. Maybe at one point the company may have in the earlier years given that going public today the market is exceptionally competitive with the similarity North Face and Patagonia. Plus you have business like Lululemon ( LULU) and Nike ( NKE) likewise completing a minimum of with some items.

Management

As kept in mind listed below Tim Boyle is the existing CEO of Columbia Sportswear. Boyle has actually been at the helm given that 1988 and if you had actually invested when Boyle brought the business public in 1998, you ‘d be one pleased financier as the stock has actually returned over a 900% return.

As you can see from these Glassdoor scores, Columbia is considered as a terrific location work and staff members at the business plainly authorize of Boyle:

Glassdoor

As my fans will understand, I’m a fan of creator led business and business concentrated on go back to investors. In spite of, the income development being below average over the last 5 years (which I’ll go over in more depth listed below), the business has actually provided investor returns as the business’s ROE is 15%, the ROCE is almost 17% and the business’s ROIC is almost 20%.

In addition, in taking a look at Columbia’s most current proxy filing, you can see Tim and Joe Boyle hold almost 40% of the business’s typical stock so there is definitely a reward to grow the share rate.

Financials

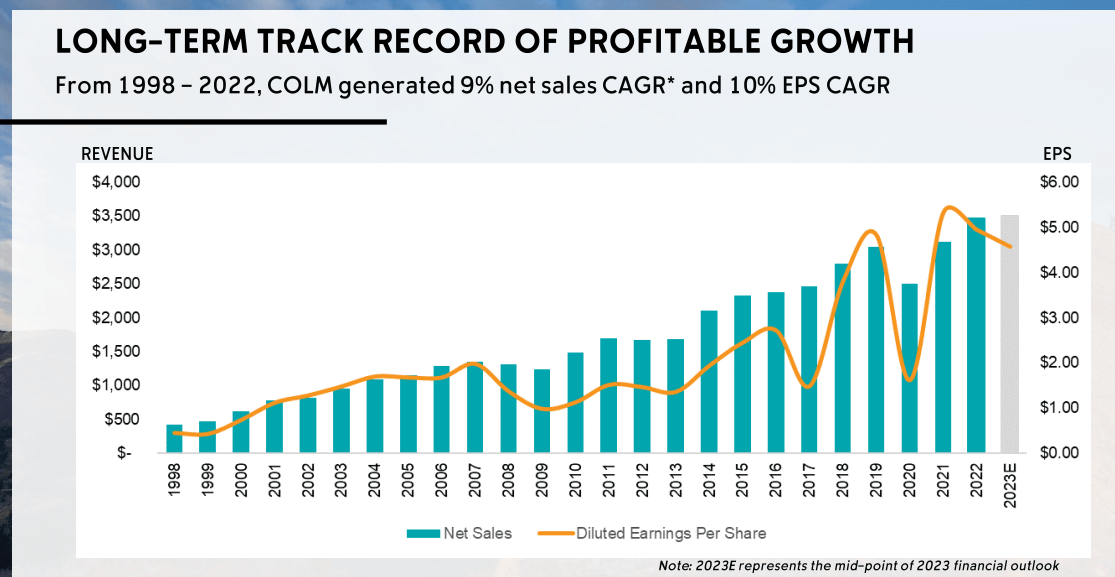

If you have actually been a long-lasting Columbia financier, you’re most likely rather occur as the business has actually created a 9% net sales CAGR given that 1998:

Financier Discussion

Nevertheless, the last 5 years have actually been various as the stock down over the most recent 5 year duration and 2023 was a battle with stock problems.

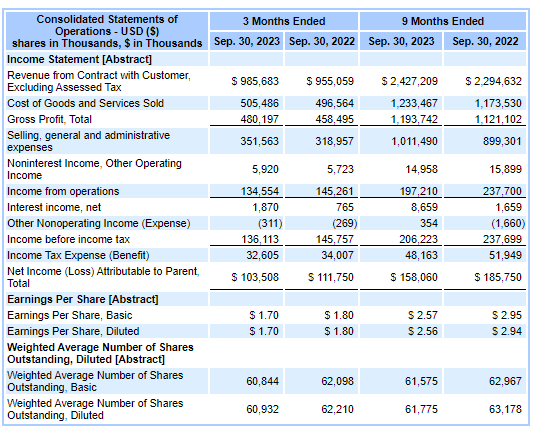

In Q3 2023, net sales can be found in at approximately $986 million which is a 3% boost compared to the 3rd quarter previous year. Nevertheless earnings was lower compared to Q3 2022 as SG&An expenditures grew 10%.

This is true for the nine-month duration too. In spite of earnings increasing and gross margin enhancing the business’s greater SG&An expenses, which management kept in mind was because of direct-to-consumer expenditures, need production financial investments and supply chain, caused lower earnings:

SEC.gov

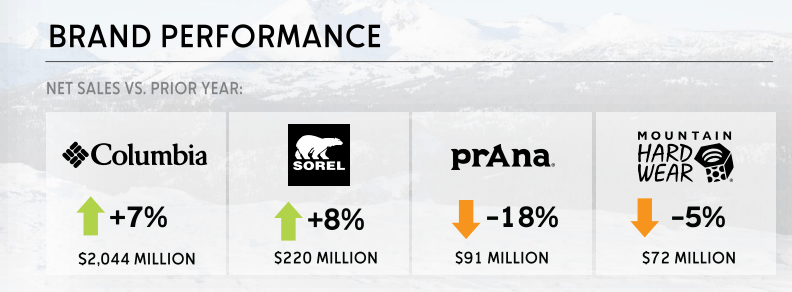

On the business’s Q3 2023 financier discussion it was kept in mind that both clothing and devices have actually increased throughout the 9-month duration which is a favorable although not all the brand names are carrying out in addition to you can see listed below:

Financier Discussion

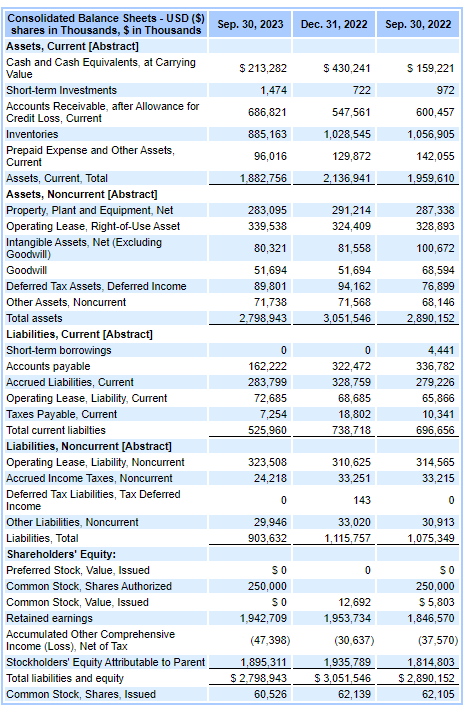

Columbia has a rock-solid balance sheet with adequate existing properties to cover all of the business’s liabilities as you can see listed below:

SEC.gov

Likewise, you can see the business’s stock levels have actually dropped. Management kept in mind the business’s stock decrease strategy is working as stock is down 16% year-over-year.

Threats

There are many dangers which the business covers in information in their 10K filing I’m going to go over 2 issues I have about Columbia.

Initially, this is an exceptionally competitive market. I believe there was less competitors when Boyle took control of today there are big rivals such as Patagonia and North Confront with numerous smaller sized gamers getting in the outside clothing market.

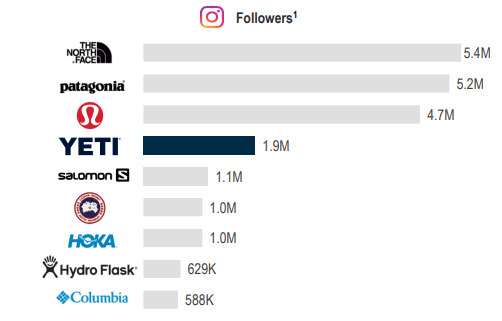

As it connects to competitors, I stress Columbia isn’t remaining pertinent. Yeti ( YETI) is a business I follow, and this is a graphic from their most current financier discussion:

Financier Discussion

As you can see Columbia is far listed below their 2 primary competitors and even listed below Yeti and the popular running brand name Hoka in regards to fans. To me this is uneasy as it reveals the business does not have insight relating to the value of social networks and having your brand name show up and pertinent.

Management and technique are my next issue. There is no doubt Tim Boyle has actually done an outstanding task throughout his period as the stock’s efficiency given that Columbia’s IPO shows Nevertheless, Tim remains in his 70’s now and will not remain on permanently. Will his child take control of or will a specific outside the household lastly run the company? I’m a long-lasting financier and therefore having a brand-new CEO take control of in the next 3-5 years with various prioritizes or techniques might substantial change one’s financial investment thesis.

Assessment

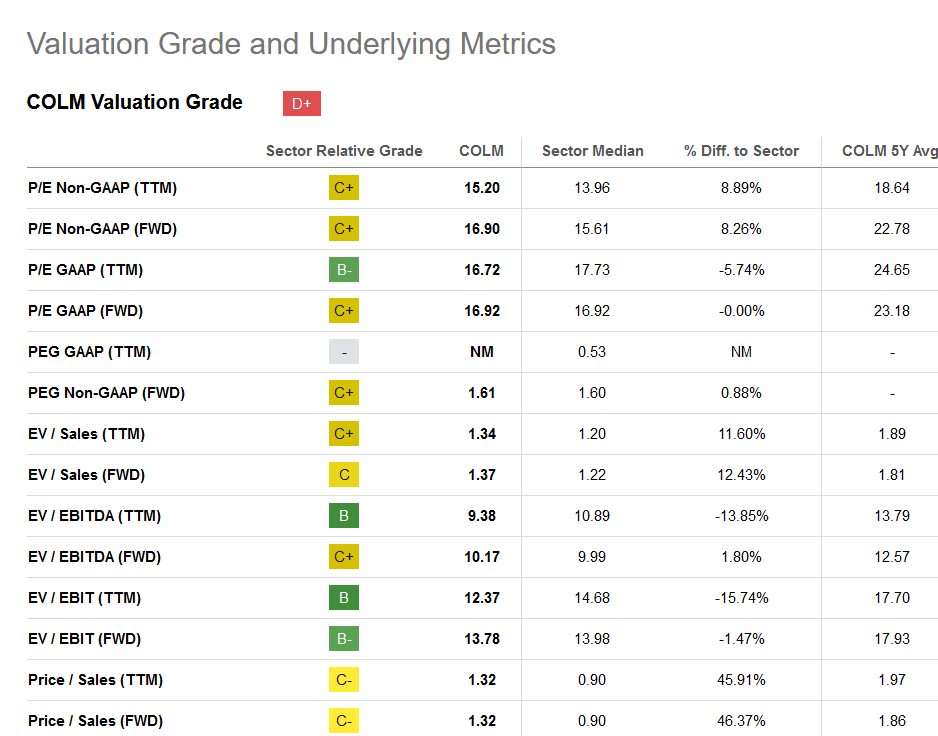

As you can see from the listed below evaluation metrics from Looking for Alpha, the general worth grade for Columbia is a “D+.”

Assessment

I really believe Columbia appears affordable. Utilizing a reverse affordable capital design with a reduced rate of 10% and a terminal rate of 3% and presumed development of 8% I concern approximated intrinsic worth of approximately $94 a share:

Brian Feroldi

Now 8% development for a business such as Columbia may be aggressive. The business kept in mind they were going for 7-9% development in the next 3 years. Nevertheless, even if you utilize 6% or 7% the approximated intrinsic worth of the share rate is higher than today’s worth.

Conclusion

Columbia is not a stock for all financiers. I do believe the business Tim Boyle has actually run given that the 1980’s will not see the kind of development experienced in the previous years. There is just excessive competitors.

Nevertheless, I do believe Columbia has numerous positives. The business has a terrific balance sheet and as management noted it will continue to reward financiers by paying dividends and redeeming shares.

Columbia makes exceptional items and as long as a Boyle runs the business, I ‘d wager that continues as the household has a substantial variety of shares of the business.

If you’re trying to find development this isn’t the stock for you however if you’re wanting to protect capital, make a dividend and sleep simple during the night then Columbia is a business to include at these affordable worths.