DNY59

The Energies Select Sector SPDR ETF ( NYSEARCA: XLU) is a premium ETF administered by State Street Global Advisors. XLU is benchmarked versus the Utilities Select Sector Index, incepted in December 1998, offering financiers a chance to buy a well-diversified utilities-focused ETF.

XLU offers financiers direct exposure to numerous styles within the sector. These consist of “electrical energy, water energy, multi-utility, independent power, sustainable electrical power manufacturers, and gas energy markets.” As an outcome, it’s planned for financiers thinking about a “targeted investing” method, as appealing chances provide themselves from time to time.

Energies plays are normally well-insulated versus the recessionary forces. As an outcome, financiers generally think about XLU as a protective setup strengthened by the incomes exposure in its leading holdings. XLU likewise boasts a fairly appealing dividend yield compared to the S&P 500 ( SPX) ( SPY). Appropriately, XLU last traded at a tracking twelve months or TTM dividend yield of 3.34%, well above SPY’s TTM dividend yield of 1.42%. Looking for Alpha Quant appointed an “A+” dividend grade to XLU, supporting the strength of XLU as a core holding for earnings financiers wanting to buy a well-diversified energies portfolio.

As a development financier, offered its long-lasting underperformance to SPY, I’m less thinking about including XLU to my portfolio. XLU provided an overall return of 136% over the previous 10 years, well listed below SPY’s 209% gain over the exact same duration. As an outcome, I’m just eager if I examine a substantial chance arising from a dislocation in the market, causing huge pessimism. I think such a chance got here as XLU bottomed out in October 2023.

As an outcome, I included XLU to my portfolio in mid-October 2023, expecting the worst was most likely to be over. Bearish financiers should be questioning whether I’m being delusional, including XLU in mid-October when the 10Y yield ( US10Y) broke the 5% mark in the exact same month (it has actually considering that dropped to 4.18%). XLU has actually gotten almost 17% in price-performance terms from its October lows through today’s highs. Is the marketplace incorrect? Is the marketplace insane? Isn’t the Fed expected to be greater for longer in mid-October? Didn’t the Fed state it would stay mindful about cutting rate of interest, although we have seen an ongoing normalization in inflation rates?

Constantly bear in mind that the marketplace is positive. The marketplace has magnified their bets of more rate cuts than formerly prepared for. As an outcome, I think it might describe why XLU bottomed out in October and even exceeded SPY from its October lows. By the time you check out the marketplace’s anticipation of rate cuts in the news media, you would have lost out on purchasing the most appealing risk/reward entry levels provided in XLU. For that reason, while there isn’t any doubt that XLU was damaged by the rise in long-lasting rates over the previous year, I evaluated it has actually reached substantial pessimism.

My thesis is likewise supported by the relative assessment levels in XLU’s leading constituent stocks.

| XLU Top 10 Holdings | Weight |

|---|---|

| 1. NextEra Energy Inc ( NEE) | 13.07% |

| 2. Southern Co ( SO) | 8.46% |

| 3. Duke Energy Corp ( DUK) | 7.77% |

| 4. Sempra ( SRE) | 4.93% |

| 5. American Electric Power Co Inc ( AEP) | 4.44% |

| 6. Rule Energy Inc ( D) | 4.24% |

| 7. Exelon Corp ( EXC) | 4.21% |

| 8. Constellation Energy Corp ( CEG) | 3.89% |

| 9. PG&E Corp ( PCG) | 3.87% |

| 10. Xcel Energy Inc ( XEL) | 3.67% |

XLU leading 10 holdings. Information source: Looking for Alpha

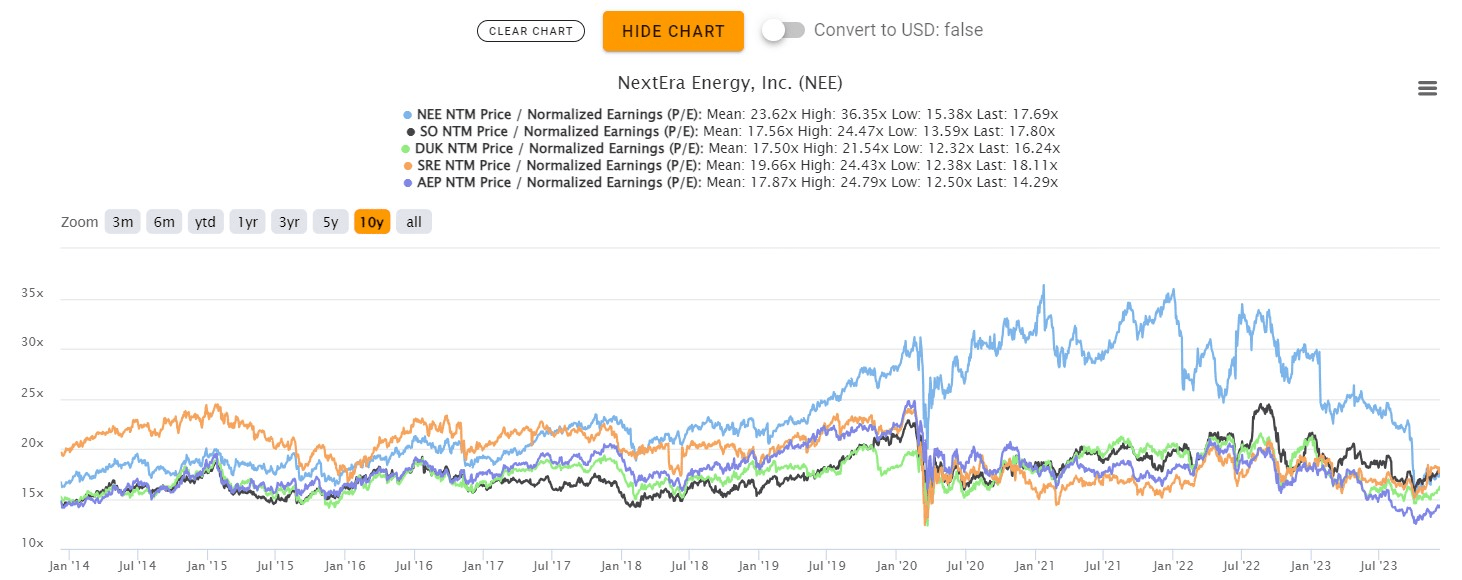

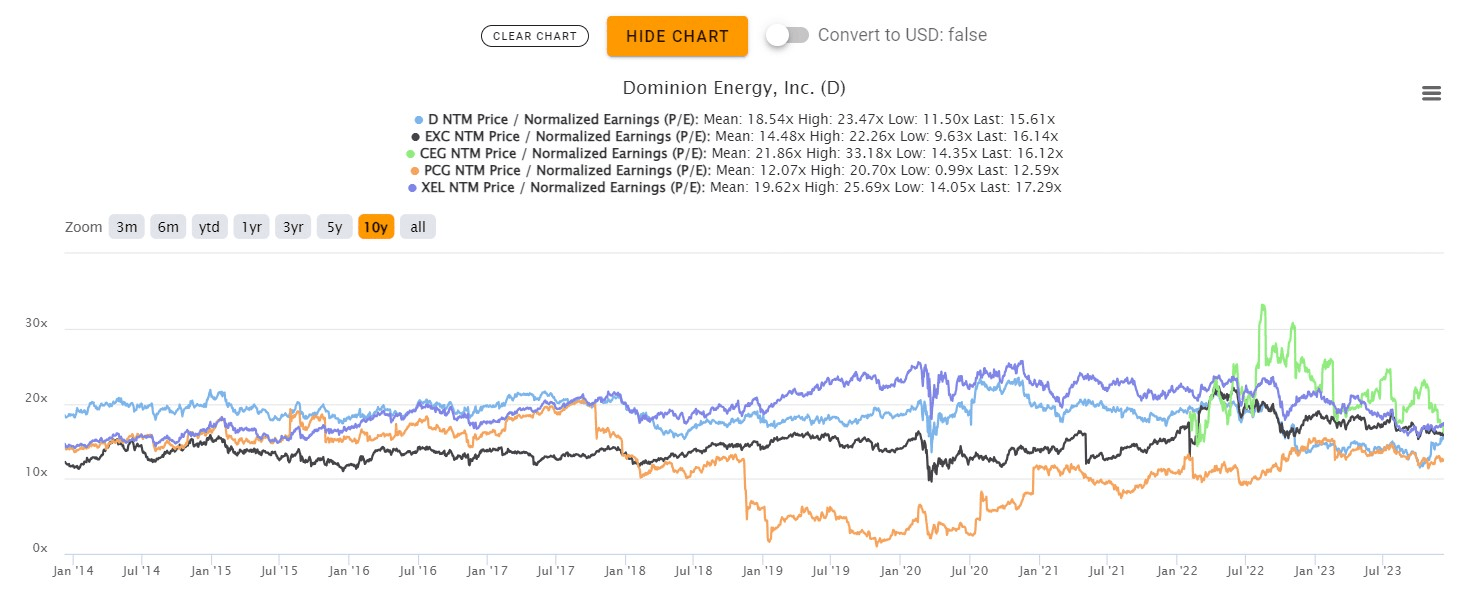

The leading 10 holdings in XLU consist of almost 60% of the fund’s weighting. As an outcome, paying attention to their relative efficiencies might be informing. XLU last traded at a forward stabilized P/E of 15.5 x, well listed below the sector’s 10Y average of 21.2 x.

XLU leading 10 holdings assessment (1/2) ( TIKR) XLU leading 10 holdings assessment (2/2) ( TIKR)

As seen above, 7 out of the leading 10 holdings last traded listed below their 10Y stabilized P/E averages, recommending relative undervaluation. Morningstar’s assessment price quotes recommend the energies sector stays 9% listed below its reasonable assessment, supporting my thesis.

Reinforced by less extreme rates of interest headwinds that impacted XLU considering that it peaked in September 2022, I think the mean-reversion thesis to close the relative underperformance space versus SPY is past due.

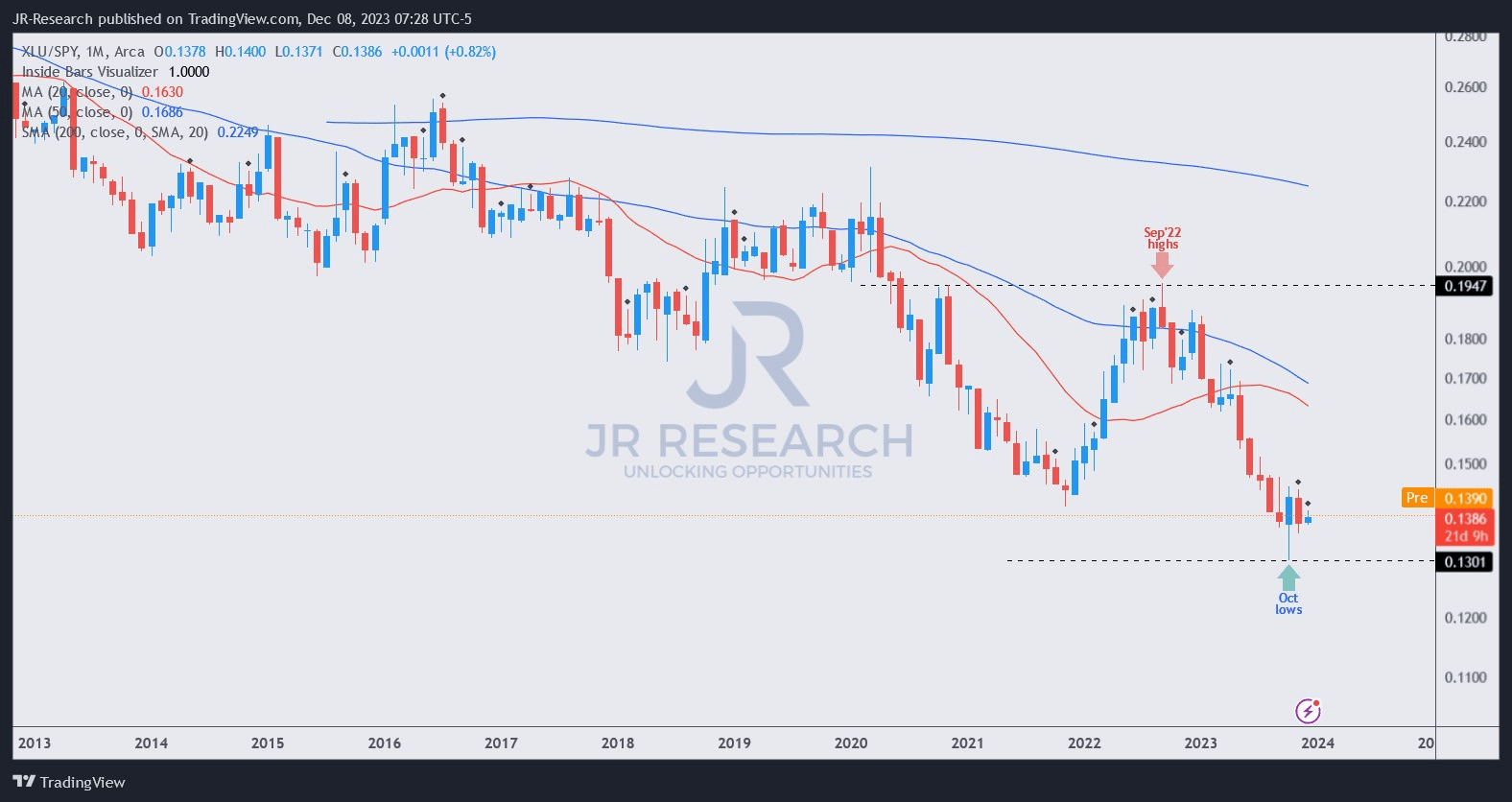

XLU/SPY rate chart (month-to-month) ( TradingView)

As seen above, XLU has actually combined versus SPY considering that it bottomed out in October 2023 and even exceeded from its lows. Nevertheless, the rise in SPY has actually likewise resulted in increased risk-on relocations as financiers turned strongly into risk-on plays.

Nevertheless, I evaluated the bear trap or incorrect disadvantage breakdown ( see rate action glossary) in XLU/SPY was verified in October. As an outcome, financiers who missed out on including XLU’s current lows ought to think about profiting from its debt consolidation before financiers turn out of risk-on sectors back into protective ones, taking earnings as tech stocks rise.

Please do not wait till the coast is clear before putting capital to operate in battered sector ETFs like XLU, as the risk/reward may no longer be so appealing at that point.

Score: Start Purchase.

Crucial note: Financiers are advised to do their due diligence and not depend on the details supplied as monetary suggestions. Please constantly use independent thinking and note that the score is not planned to time a particular entry/exit at the point of composing unless otherwise defined.

We Wished To Speak With You

Have positive commentary to enhance our thesis? Found a crucial space in our view? Saw something crucial that we didn’t? Concur or disagree? Remark listed below with the goal of assisting everybody in the neighborhood to find out much better!