mixmotive

Summary

S&P Global ( NYSE: SPGI) had an effective 1Q23, in my viewpoint, with earnings, EBITDA margins, and EPS all going beyond agreement price quotes. This was mainly due to the Rankings company, which did better than anticipated. The Rankings section earnings visited just 5%, a substantial enhancement from the previous quarter and 600 bps much better than Moody’s ( MCO) Investors Service section’s 11% earnings drop. Thinking about SPGI’s increased refinancing and M&An offer circulation, in addition to the truth that in 2015 was a simple contrast, I stay positive that scores will enhance in the coming quarters. Things would be even much better for SPGI if rates of interest dropped in 2H23. My thesis that SPGI is amongst the very best companies on the planet stays the same. I repeat my Buy score

Rankings

Although the Rankings section fell by 5%, it substantially exceeded both agreement price quotes and MCO this quarter. Within this, Transactional scores earnings, which represented simply under half of Rankings earnings, visited a reasonably modest 6% in 1Q23. SPGI’s strong execution and outperformance in Structured items assisted add to this outstanding outcome, I think, as earnings visited just 3% compared to MCO’s 31%. The rest of SPGI’s section earnings originates from sources aside from deals, and those earnings fell by 4%. This earnings stream is weaker in nature due to its cyclicality; therefore, a decrease in the low single digits was better than I anticipated. I believe the marketplace is currently method past the weak IR environment, evaluating by the appraisal and share cost motion, both of which have actually recuperated over the previous 2 months. The focus here is 2H23 and beyond, where I anticipate to see an enhancement completely year deal earnings as I believe the marketplace will see a healing in M&An offers (appraisal get less expensive), and more refinancing activities (as rates remain flattish or down). My view is likewise strengthened with management self-confidence that on the transactional side, where billed issuance assistance for FY23 has actually been increased to 3-7% y/y from a preliminary guide of 2-6% y/y.

Synergies

In addition noteworthy is the truth that SPGI is pressing ahead on anticipated synergies from the merger with IHS Markit The run-rate expense synergies reached $552 million in 1Q23, which is practically 90% of the overall expense savings (FY23 target of $600 million) prepared, showing unbelievable focus from management on providing the anticipated synergies, particularly on the expense front. There is a high possibility that synergies will be recognized in 2Q23 at this rate. On the earnings side, nevertheless, things are still getting rather gradually, a pattern I associate in part to the slow macro. In contrast to the $350 million objective set for FY26, run-rate earnings synergies have actually now reached $52 million. I do not believe the sluggish speed of recognizing run-rate earnings synergies is a weak point. In specific, when it is being driven mostly by cross-selling items. I anticipate SPGI to completely understand its expense synergies ahead of its timeline, and earnings synergies to enter into sped up mode when the macro environment turned for the much better.

Negatives

The marketplace Intelligence section has actually not carried out in addition to it needs to this quarter, and I anticipate that to continue as the marketplace uses more pressure. EBIT amounted to $343 million on earnings simply over $1 billion in 1Q23. Provided the present environment of unpredictability in the banking market, management has the most cynical forecasts for both earnings and EBIT. Consumers are undoubtedly being more careful because of the unstable macro, which has actually led to a somewhat extended sales cycle, in my viewpoint. Nevertheless, it was reassuring to discover that the large bulk of offers are still developing into earnings; this suggests that need is simply being postponed instead of vanishing completely.

Assistance

My focus this quarter has actually been on whether management alters its outlook for FY23. Mid-single digit earnings development is still expected, as is an adjusted EBIT margin of 45.5% to 46.5% and changed EPS of $12.35 to $12.55. In what seems an easy restatement of previous assistance, however I think they are implicitly increasing it. The important things to keep in mind here is that SPGI sale of its Engineering Solutions system is now anticipated to close in early May instead of June. So if we represent that 1-month distinction of contribution loss, however assistance still stays the very same, we can presume that management is assisting for 1 more month of efficiency contribution from other sectors.

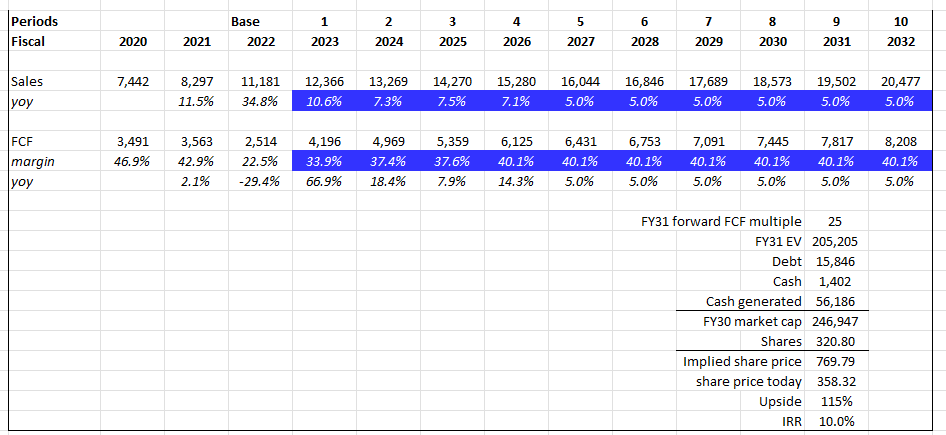

Appraisal

I have actually upgraded my design to show the most recent numbers, agreement price quotes over the next 5 years, and likewise the IRR one needs to anticipate today. Following my initiation post, which utilized a DCF to worth SPGI, I think SPGI continues to provide at extremely steady 10% IRR over the next ten years. The huge distinction in between my upgraded design vs. formerly is that I anticipate SPGI to trade at a FCF multiple of 25x. This equates to a 4% FCF yield (1/25x), which I believe is reasonable considered that rates are not likely to revert back to 0%, and SPGI needs to trade at FCF yield that is greater than the dominating rates of interest (as it has greater danger and volatility, compared to treasury expenses).

Own design

Dangers

The huge danger I am seeing with SPGI, a minimum of in the near-term, is that development is contingent on healing in refinancing and M&A activities. While I am favorable on this, the danger of the economy turning into an extremely bad economic downturn is not something that is off the table yet. Specifically with the financial obligation ceiling story drifting in the market, if the United States does default on its financial obligation, I believe it will be a significant catastrophe for the economy.

Conclusion

SPGI efficiency in 1Q23 was good, exceeding agreement price quotes and showing strength in its Rankings company. In addition, SPGI’s development in attaining expense synergies from the IHS Markit merger is outstanding, with run-rate expense savings reaching practically 90% of the target. While earnings synergies are getting gradually, the concentrate on cross-selling items bodes well for future development. Nevertheless, difficulties continue the marketplace Intelligence section due to careful client habits in the unsure banking market. Nevertheless, management preserves a favorable outlook for FY23, expecting mid-single digit earnings development. In general, my belief in SPGI as an exceptional financial investment chance stays the same, and I repeat my Buy score.