Dilok Klaisataporn

Service advancement business provide strong dividend yields to passive earnings financiers. One BDC that I have actually owned for a while which offers a high-yield along with dividend development is Golub Capital BDC ( NASDAQ: GBDC)

With the stock now costing a 2% premium to net possession worth, even the business’s robust net financial investment earnings discussion 1Q-24 and an enhancing credit pattern are not essentially enhancing the risk/reward relationship, in my view. Hold.

My Ranking History

I altered my stock category for Golub Capital from Buy to Hold 3 months back as Golub Capital’s discount rate to net possession worth vanished and the BDC needed to face the possibility of decreasing net financial investment earnings in a falling-rate environment.

With that being stated, I believe that all of Golub Capital BDC’s crucial efficiency metrics in 1Q-24 continue to support a Hold stock category.

Golub Capital’s Portfolio Is Still Growing, Improving Non-Accrual Ratio

I have actually singled out Golub Capital a variety of times in my last 2 years of composing here, mainly since the BDC is mainly concentrated on high quality First Liens that, in my view, restrict the threat of purchasing this BDC in case of an economic downturn.

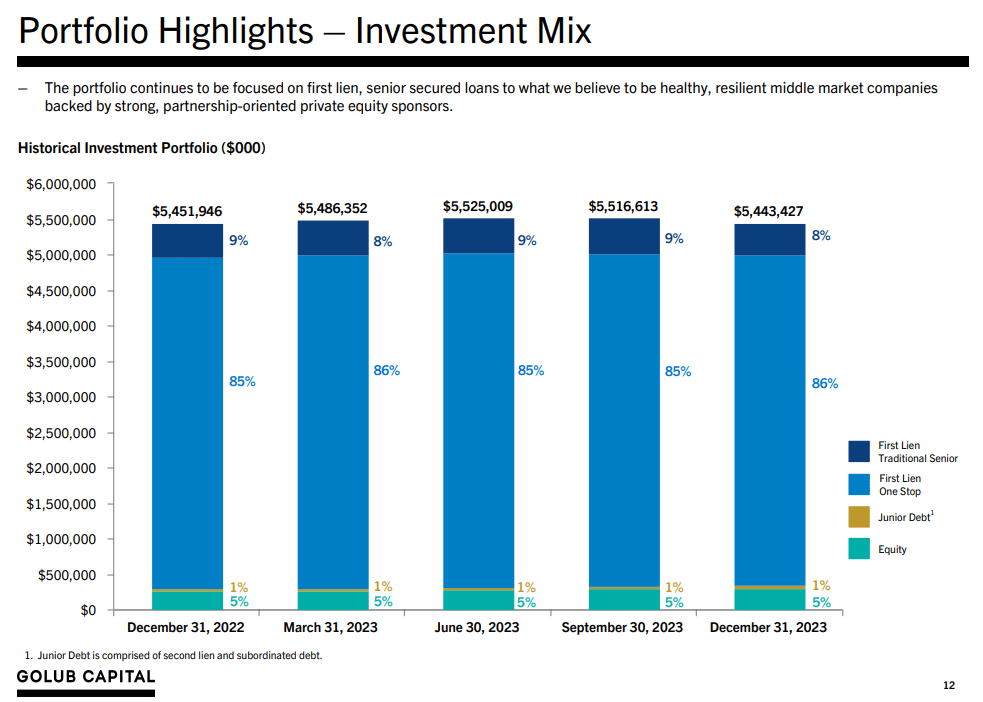

At the end of 2023, Golub Capital was to 94% bought Very first Liens which is among the greatest portions bought this loan classification that I have actually ever encountered.

Golub Capital’s Portfolio worth at the end of 2023 was $5.4 billion that made it the sixth-biggest BDC by net possessions in the market.

This is what Golub Capital’s portfolio at the end of 2023 appeared like.

Portfolio Emphasizes – Financial Investment Mix ( Golub Capital BDC)

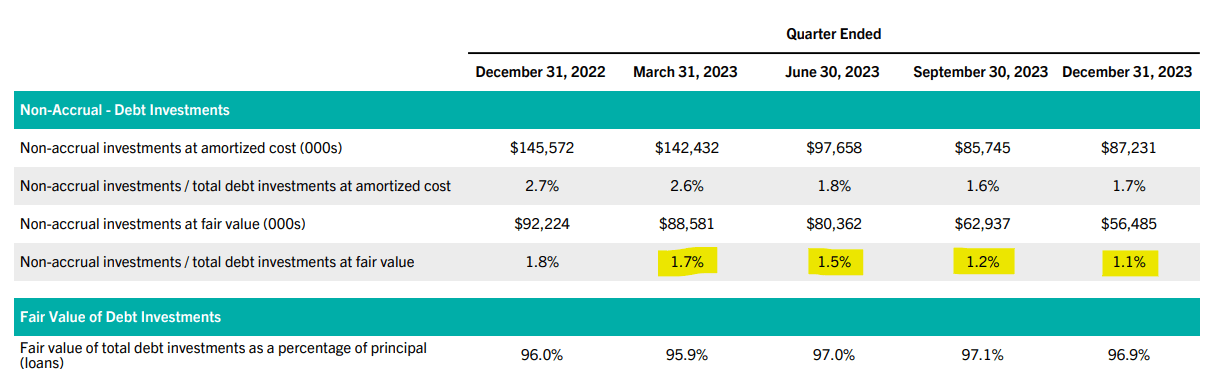

Though the portfolio has actually not grown in 1Q-24, Golub Capital had another win as far as its non-accrual circumstance was worried. The BDC’s non-accrual ratio, which is determined as a portion of overall financial obligation financial investment reasonable worth decreased 0.1 portion indicate 1.1% at the end of 2023.

The BDC’s non-accrual ratio has actually dropped 4 quarters in a row in 2023 and the pattern is for that reason extremely favorable. At the end of 4Q-23, Golub Capital had 9 financial investments on non-accrual status which was the same from the previous quarter.

Non-Accrual Ratio ( Golub Capital BDC)

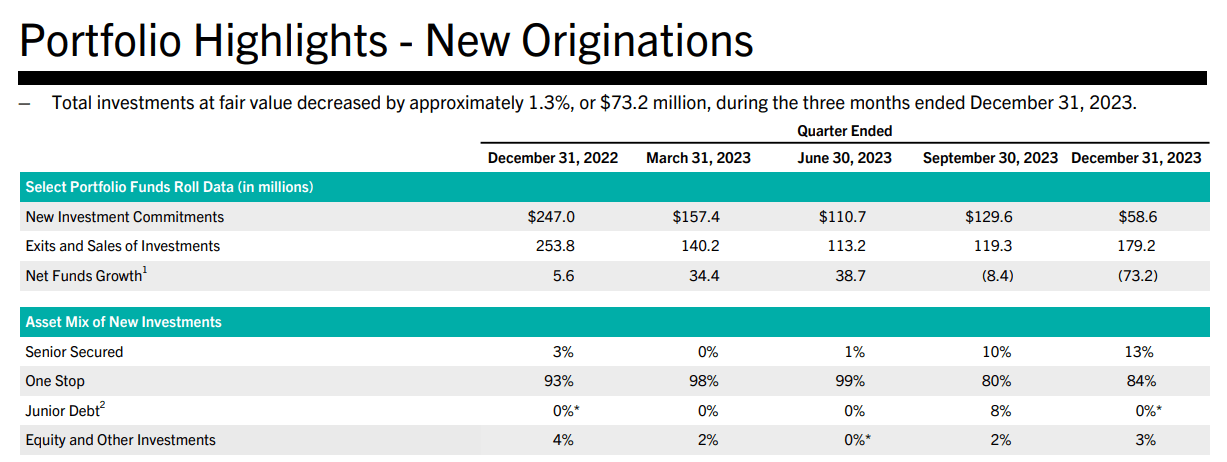

Though the credit quality pattern was motivating and plainly a favorable conclusion from Golub Capital’s revenues release, the very same might not be stated about the business’s portfolio development. It was the 2nd quarter in a row in which Golub Capital’s portfolio decreased due to a high variety of sped up payments and loan sales and a weak origination environment.

This pattern, nevertheless, ought to be anticipated to reverse in 2024 if the reserve bank slashes its short-term rate of interest, consequently making Very first Liens more affordable for customers. Practically all brand-new originations in 1Q-24 were Senior Guaranteed Very First Liens.

Portfolio Emphasizes – Brand-new Originations ( Golub Capital BDC)

2 Raises In 2023, Excess Protection Permits 2024 Dividend Walking

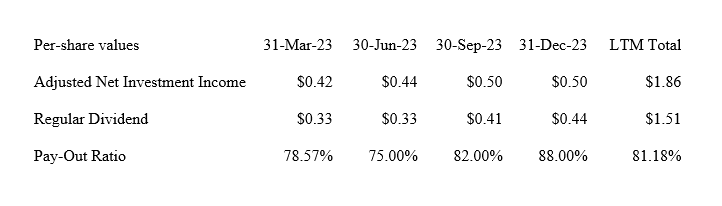

Taking A Look At Golub Capital’s dividend protection metrics for the 4th quarter it emerges that the BDC continues to have a great deal of capacity for dividend development in 2024.

The BDC handed passive earnings financiers 2 dividend boosts in the 2nd half of 2023 by raising its routine dividend 12% in 3Q-23 to $0.37 per share and paying an overall of $0.07 per share in extra dividends.

Golub Capital likewise raised its 1Q-24 routine dividend to $0.39 and revealed an additional dividend of $0.07 per share in extra dividends which raises the leading dividend yield to 11%.

Golub Capital’s net financial investment earnings results for 2023, pay-out development and dividend pay-out ratio can be seen in the table listed below.

Dividend ( Author Developed Table Utilizing BDC Details)

Buy On Dips, However Not Now

As I have stated sometimes previously, I have a hostility for paying more than net possession worth for a BDC, no matter how excellent the dividend or how low the pay-out ratio is.

Due to its excess dividend protection and the main concentrate on First Liens, Golub Capital, nevertheless, is a leading BDC for me to purchase on dips and the BDC is still a core holding in my passive earnings portfolio.

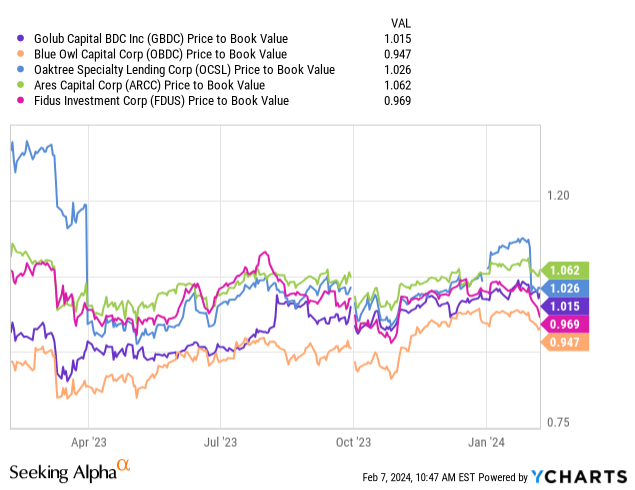

I currently see a strong, opportunistic purchasing chance in Oaktree Specialized Loaning Corporation ( OCSL) which revealed recently a wear and tear in its loaning efficiency, setting off a significant drop in the BDC’s stock rate.

Normally speaking, I cut down on my BDC purchases when the stock trades at a premium, however when it comes to Golub Capital I ‘d think about including listed below net possession worth $15.03 (my long-lasting stock rate target).

Golub Capital was offering listed below net possession worth for much of 2023, however has actually re-rated to net possession worth recently due to the BDC being placed to benefit from greater portfolio earnings associated with its floating-rate financial obligation financial investment portfolio.

Golub Capital’s floating-rate direct exposure is 99%. In my view, Golub Capital is priced at intrinsic worth today and considering that I am hardly ever ready to pay complete rate for a BDC’s yield, I believe that a Hold stock category is the very best strategy here.

With that stated, a dip listed below net possession worth would make the BDC a lot more engaging once again from an evaluation, security margin and dividend yield viewpoint.

Why I Might Be Off And Golub Capital’s Stock May Re-Rate Greater

Golub Capital is a 99% floating-rate BDC, so the reserve bank might toss a wrench into the business’s net financial investment earnings possible when rates boil down.

A higher-for-longer rate environment could, nevertheless, raise the BDC’s net financial investment earnings capacity and permit the payments of extra dividends that might improve the BDC’s efficient yield. The very best method to handle these dangers is to remain neutral and gather the dividends.

My Conclusion

Golub Capital is an extremely well-managed BDC with a Very first Lien focus that I value a lot and would value much more throughout an economic downturn when default dangers are on the increase.

As far as the efficiency examination opts for Golub Capital’s 1Q-24, the BDC continued to outearn its dividend with net financial investment earnings and the credit quality pattern enhanced. As much as I like the earnings that I produce from Golub Capital’s stock, I do not believe that the BDC is a specific take.

Remaining invested or waiting on the sidelines up until a purchasing chance emerges (listed below $15.03) might be the very best strategy here. Hold.